financial wellness

More Americans Joining Workforce, But Many Are Unable to Find Living-Wage Jobs

Last Updated on September 19, 2025 by Daily News Staff

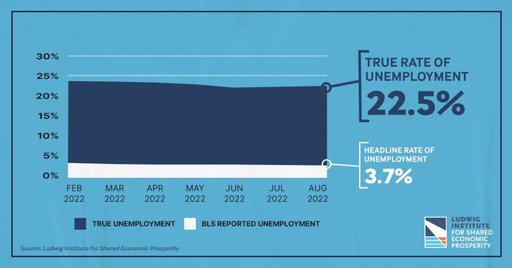

WASHINGTON, Sept. 15, 2022 /PRNewswire/ — The American workforce expanded from July to August, but many of those workers found they were unable to secure Living-Wage Jobs, according to an analysis by the Ludwig Institute for Shared Economic Prosperity (LISEP).

In its monthly True Rate of Unemployment (TRU) for August, LISEP reported that 22.5% of American workers are now classified as “functionally unemployed,” defined as the jobless, plus those seeking but unable to secure full-time employment, even if they want to work full-time and/or cannot earn above the poverty line after adjusting for inflation. This is an increase of 0.2 percentage points over the July TRU.

TRU’s sister metric, TRU Out of the Population (TRU OOP) – a measure of those who are functionally unemployed out of the entire population, not just active workforce participants – remained unchanged, which, when coupled with a rising TRU, indicates more workers are joining or returning to the labor force.

“It is a net positive that previously discouraged workers are rejoining the workforce, but unfortunately, their return to the workforce is, in many cases, not a return to full-time, living-wage employment,” said LISEP founder and chair Gene Ludwig. “The challenge for policymakers is to continue to encourage positive growth in employment opportunities, but do so in a manner that provides for growth in living-wage jobs for every American who wants one.”

Demographically, Black workers saw the biggest jump in TRU, increasing by 0.6 percentage points, from 25.8% to 26.4%. This, with the Black TRU OOP climbing by 0.7 percentage points, indicates that a larger percentage of Black workers are classified as functionally unemployed. Hispanic workers saw no change in the TRU, holding steady at 26.3%, with White workers tracking the overall TRU and increasing by 0.2 percentage points, to 20.7%. Male TRU increased a full percentage point, from 17.5% to 18.5%, while women dropped a half percentage point, from 27.5% to 27.0%.

Living-wage job opportunities continue to be an issue for workers with only a high school diploma, with the TRU for this group jumping 2.5 percentage points, from 24.5% to 27.0%. Likewise, those without a high school degree saw their TRU increase, from 47.3% to 47.6%. TRU for workers with some college (but no college degree) dropped, from 25.6% to 23.7%, but an analysis of the TRU OOP for this group indicates the decline is likely due to discouraged workers in this cohort leaving the workforce.

“We know the cost of living continues to be an issue for low- and middle-income Americans, as inflation continues to erode the ability of these workers to maintain even a basic standard of living. So in that respect, I’m somewhat relieved there wasn’t a bigger increase in the overall TRU,” Ludwig said. “But at the same time, we are witnessing an alarming decline in the opportunities for some minority workers to earn a living wage, which is undoubtedly a reason for concern. The bottom line: we can do better.”

About TRU

LISEP issued the white paper “Measuring Better: Development of ‘True Rate of Unemployment’ Data as the Basis for Social and Economic Policy” upon announcing the new statistical measure in October 2020. The paper and methodology can be viewed here. LISEP issues TRU one to two weeks following the release of the BLS unemployment report, which occurs on the first Friday of each month. The TRU rate and supporting data are available on the LISEP website at https://www.lisep.org/tru.

About LISEP

The Ludwig Institute for Shared Economic Prosperity (LISEP) was created in 2019 by Ludwig and his wife, Dr. Carol Ludwig. The mission of LISEP is to improve the economic well-being of middle- and lower-income Americans through research and education. LISEP’s original economic research includes new indicators for unemployment, earnings, and cost of living. These metrics aim to provide policymakers and the public with a more transparent view of the economic situation of all Americans, particularly low- and middle-income households, compared with misleading headline statistics.

About Gene Ludwig

In addition to his role as LISEP chair, Gene Ludwig is founder of the Promontory family of companies and Canapi LLC, a financial technology venture fund. He is the founder and CEO of Ludwig Regulatory Group (LRG), which advises financial firms on critical matters. Ludwig is the former vice chairman and senior control officer of Bankers Trust New York Corp. and served as the U.S. Comptroller of the Currency from 1993 to 1998. He is also author of the book The Vanishing American Dream, which investigates the economic challenges facing low- and middle-income Americans. On Twitter: @geneludwig.

SOURCE Ludwig Institute for Shared Economic Prosperity

Lifestyle

Get Your Kids Ready to Go Back-to-School with Affordable Health Coverage

Once school starts, life moves fast. There is homework, practices, permission slips, and early mornings. Before the calendar fills up, take a moment to make sure your child has affordable health coverage for the year ahead.

Get Your Kids Ready to Go Back-to-School with Affordable Health Coverage

(Feature Impact) Once school starts, life moves fast. There is homework, practices, permission slips, and early mornings. Before the calendar fills up, take a moment to make sure your child has health coverage for the year ahead.

Free or low-cost health coverage is available through the Children’s Health Insurance Program (CHIP) or Medicaid in your state for eligible individuals. With health coverage, your kids and teens can get the care they need to stay healthy and do well in school.

Think your family might not qualify? You might be surprised. Many families may qualify for coverage without realizing it! Eligibility varies by state and is based on family income and household size. In most states, children up to age 19 from a family of four earning up to $80,000 per year may be eligible. In some states, eligible children can still qualify if family income is even higher.

Getting your child covered helps you get them the health care they may need. When a child is sick, the right medicines help them get back to school. If a child has a tough time focusing, there are supports to help. If your child does not see as well as other children, these programs cover glasses. Healthy kids are confident kids, who are ready to participate in every opportunity inside and outside the classroom!

Why Health Coverage Belongs on Your Kids’ Back-to-School List

Having health coverage can help families, like yours, to send your kids and teens off to school ready to learn. Depending on the program and a child’s individual needs, Medicaid and CHIP can provide eligible kids up to age 18 (Medicaid) or 19 (CHIP) with a range of services to support their health all year long, such as:

- Annual checkups and school physicals to prepare children to learn, play, and participate.

- Preventive care to identify health needs early and keep children healthy throughout the year.

- Dental care to help prevent tooth aches, cavities, and missed school days.

- Vision and hearing services to support learning and classroom participation.

- Mental health care to support emotional well-being and school success.

- Prescription medications and treatment to help manage symptoms and stay on track.

- Specialized services for children with disabilities to support growth and learning.

How to Apply

You can apply for Medicaid and CHIP in many ways:

- By phone

- By mail

- In-person through your state’s Medicaid or CHIP office

- Or find your state’s information online at InsureKidsNow.gov/coverage.

Act now to get your child covered before they need health care. Enrollment for these programs is open year-round, meaning families do not have to wait for a specific time of year to get covered.

Once enrolled, coverage must be renewed every twelve months, so it is important to keep your address, email, and phone number up to date with your state Medicaid or CHIP office to avoid missing important renewal information. Visit InsureKidsNow.gov or call 1-877-KIDS-NOW (1-877-543-7669) for more information.

Information provided by the U.S. Department of Health & Human Services. This communication was printed, published, or produced and disseminated at U.S. taxpayer expense.

Photo courtesy of Shutterstock

SOURCE:

Centers for Medicare and Medicaid Services

💪 Your health journey starts here! Explore the latest health news, fitness tips, wellness trends, and healthy living advice. Share your thoughts in the comments and subscribe to the STM Daily News newsletter to stay informed and inspired every day.

financial wellness

Building Brighter Futures: Helping Young People Succeed in a Changing Economy

Changing Economy: During a time when the economy is changing rapidly and shifting the landscape of work into uncertain territory, academic success is no longer enough to put young people on a stable path to the future. Smart students need to start taking steps in new directions, adding key concepts like financial literacy, economic mobility and entrepreneurship to their knowledge arsenals.

Building Brighter Futures: Helping Young People Succeed in a Changing Economy

(Feature Impact) During a time when the economy is changing rapidly and shifting the landscape of work into uncertain territory, academic success is no longer enough to put young people on a stable path to the future. Once, a high school diploma was enough to land a well-paying job. Then a college degree became the gold standard. Now the roadmap has changed again, which means that smart students need to start taking steps in new directions.

According to Junior Achievement, three key concepts to add to modern teenagers’ knowledge arsenal include financial literacy, economic mobility and entrepreneurship.

Why Financial Literacy Matters

When young people are equipped with the knowledge they need to earn, manage, save and invest money, it supports their journey through every life milestone ahead, from education and homeownership to retirement and more. Financial literacy gives people the confidence to make smart decisions while dodging costly mistakes like getting into high-interest debt.

A recent Junior Achievement survey indicated that although 42% of Americans struggle with money management, 23% feel their income could be sufficient if they understood how to manage it more effectively. Giving students a strong foundation in financial literacy can set them up well to not only earn money but use it wisely to meet their future needs and accomplish their goals.

The Power of Economic Mobility

Economic mobility refers to the idea that each generation can expect to achieve better opportunities and more financial stability than the one before. Today’s youth are growing increasingly skeptical of this possibility, and for good reason: they see that even many college graduates are underemployed and struggling to find their feet.

There’s no denying the game has changed. However, upward economic mobility is still within reach for students who are willing to learn the new rules, especially if they have parents and educators supporting their journeys. With or without a college degree, students who engage with their communities, believe in their own potential and focus on building transferable personal and entrepreneurial skills can find themselves well-positioned to navigate a changing world.

How to Grow Entrepreneurial Skills

Topics like financial literacy and business acumen can be taught in a variety of ways both in and out of the classroom. Other key entrepreneurial skills – like leadership, confidence, work ethic, creativity and critical thinking – are more like muscles that get stronger when they’re trained. While academics are still important, hands-on opportunities and experiences are invaluable parts of the equation to prepare students for economic success.

Take programs like Future Bound by Junior Achievement, for example, which is an immersive annual event designed to empower high school students with essential skills and opportunities to innovate. Participants put their intelligence, creativity and ambition to the test during four team competitions where they can showcase and hone real-world business and economic skills. Winners receive national honors, awards, scholarships and prizes from event sponsors, including Pacific Life Foundation and Staples, among others. Plus, all attendees get the chance to network with industry leaders from around the country, participate in workshops and connect with other future-focused teens.

Whether you’re a student, parent, educator or volunteer, explore more resources to help young people succeed at JA.org.

Photo courtesy of Shutterstock

SOURCE:

📰 Enjoying STM Daily News? Join the conversation!

💬 Leave a comment, share your thoughts, and subscribe to our newsletter for the latest stories, updates, and “News You Can Use This Moment!” delivered to your inbox.

Stay connected with STM Daily News!

Consumer Corner

Deed fraud can cause vulnerable Detroiters to lose their homes – here’s why it’s hard to catch the thieves

Deed fraud is rising in Detroit, where forged deeds can strip vulnerable homeowners of their property. Here’s how title theft works, why it’s hard to catch, and what reforms could help.

Donovan McCarty, Michigan State University

Buying her first home on Detroit’s far east side in 2021 was the moment when a lifelong dream finally came within reach for Kim Page.

“I accomplished something that I always wanted to do,” said Page, who grew up in the city. “I always wanted to buy my own home since I was like 18. I never wanted to rent from anyone.”

Page said she had saved US$15,000 and used $3,800 in cash to buy the single-family brick house on Britain Street. The house, owned by a friend planning to move out of Detroit, was “damaged pretty bad,” Page recalls. But the house was hers to care for, and she was determined to fix what was broken.

For the next several years, Page poured her sweat and paychecks into the property. Working first as a welder at automotive supplier Fisher Dynamics, and later as a phlebotomist, she paid for a dumpster, windows, a door, ceiling repair and an awning above her front porch. Page invested $27,000 in needed repairs and, in 2022, happily moved in.

But in August 2023, a storm damaged her roof. By March 2024, mold had grown inside the property, which made Page struggle to breathe; she moved in with family. She returned to the home in April 2024 for an appointment with a representative from the Federal Emergency Management Agency. That’s when Page noticed the locks had been changed. Perplexed but undeterred, she broke down the back door to get inside and purchased new locks, which she installed.

Then on a hot, summer day in July 2024, Page came home to discover all her locks had been changed again.

Searching for answers, Page called the Wayne County Register of Deeds’ Mortgage and Deed Fraud Unit. The staff confirmed she was a victim of deed fraud – a crime where scammers forge signatures to record a phony transfer of property ownership. Once criminals hijack the title, they can sell the property, rent it out or drain its equity with mortgages, potentially leaving the rightful owner to face the legal and financial fallout.

“I just was in shock,” Page said. “I can’t believe somebody really did this to me.”

A nationwide problem that’s hard to nail down

Page reached out to me for help in March 2025. I’m a housing attorney, assistant professor at Michigan State University College of Law and director of the Housing Justice Clinic. I have represented dozens of victims of deed fraud.

I have also studied how property recording systems respond – or, more accurately, fail to respond – to fraud. My work examines how procedural gaps in title systems disproportionately harm elderly, low-income and minority homeowners.

Nationwide, deed fraud – also called quit claim deed fraud or home title theft – is a growing problem, including in New York, Boston, Miami and Philadelphia.

Exactly how big a problem it is, is hard to know. The FBI does not track deed fraud specifically, instead grouping it into a larger category of real estate crimes.

From 2019 through 2023, 58,141 victims in the U.S. reported $1.3 billion in losses relating to real estate crime, the FBI says. However, that number is likely undercounted because many people don’t know where to report it, are embarrassed they were victims or don’t know yet they have been targeted.

In Detroit, deed fraud may be particularly prevalent because so many housing deals are made in cash and many properties owe back taxes. The Wayne County Mortgage and Deed Fraud Unit has tracked more than 13,000 inquiries regarding deed fraud and has opened over 2,300 cases throughout Wayne County since 2005.

Without oversight, the crime often goes undetected

Committing deed fraud is remarkably simple.

A deed is the legal document that transfers ownership of a home or other real property from one person to another. When a home is bought or sold, a deed is legally drawn up to reflect the transfer of ownership. That deed is then recorded with a county register of deeds, providing public notice of who legally owns the property.

A fraudster can forge the signature of the real owner – sometimes someone who is deceased. They can file a deed that appears valid on its face but isn’t.

They then record that false deed with a county register of deeds, the local government office that keeps public land records and other documents showing ownership, claiming title to property they do not actually own.

Fraudsters often target vulnerable people and properties, including elderly owners, families dealing with inherited homes, and houses that appear vacant or neglected, such as those behind on property taxes.

The incentive is clear: Once a fraudster appears to hold title, they can try to sell the property to an investor or an unsuspecting buyer looking for stable housing. I have seen fraudsters secure as much as $50,000 from one deal when they obtained a mortgage based on a fraudulent deed. One notable case of fraud targeted Elvis Presley’s former estate, Graceland.

In Michigan and most other states, recording offices do not have authority to substantively review a deed to determine whether it is fraudulent. If the document complies with technical formatting requirements, such as margin and font size, it must be recorded. Once stamped and indexed, the deed appears legitimate and can easily trick desperate buyers, investors, financial institutions and even police officers, lawyers and judges.

In other words, the recording process is largely administrative, not investigative. The government office accepts and files the document without first verifying that the person signing it actually had the legal right to transfer the property.

That means a fraudulent deed can enter the public record, look valid to the outside world and remain undiscovered for months or even years.

Detroit is vulnerable

The housing market helps explain why Detroiters are more vulnerable to deed fraud.

Homes in Black neighborhoods nationwide are systematically undervalued compared with similar homes in white neighborhoods. Black borrowers are also more likely to be denied conventional mortgage loans. Detroit is about 73% Black, with a median household income of roughly $39,000 and a poverty rate exceeding 30%.

In a market where access to traditional financing is uneven and home prices are relatively low, cash sales accounted for 4 in 10 sales in February 2024.

Lenders, brokers and title companies act as informal gatekeepers when people purchase a home using a mortgage. In cash sales, those actors are absent, and there are fewer opportunities to detect irregularities in the documented history showing how title passed from one owner to the next over time.

Illegal tax practices led to thousands of foreclosed homes

Property tax distress attracts fraudsters. Fraudsters seem to rely on publicly available tax foreclosure lists to identify properties that appear abandoned. They then pay the past-due taxes to remove the property from foreclosure and attempt to sell or mortgage the property using their fraudulent deed.

The fraudsters may also assume that the owner lacks the resources to wage a prolonged legal fight to recover title if they do uncover their scheme. In many cases, that assumption proves correct.

Michigan’s Constitution caps assessments at 50% of market value, but researchers have found that from 2009 to 2015, a majority of Detroit homes were assessed above that limit. Once those inflated bills went unpaid, interest, penalties and fees accumulated, often ending in tax foreclosure.

More than 100,000 Detroit residents lost homes in that crisis, and homeowners were overtaxed by at least $600 million between 2010 and 2016.

In a city already destabilized by unlawful tax foreclosure, fraudsters found opportunity in homes burdened by vacancy and broken chains of ownership.

The burdens that deed fraud victims face

My first encounter with deed fraud came in July 2023. I received a request for legal assistance from a man who said he had been evicted from a home he claimed to own. Honestly, I didn’t believe him.

But when I pulled the court records and deeds, I learned he was right.

A fraudulent deed had been filed on his property, stripping him of title. The fraudsters then filed an eviction case against him.

The owner had no phone and no internet access to attend the virtual hearings. The court entered a judgment to evict him. A bailiff came, broke down his door and threw his belongings into a dumpster.

It took six months and two separate court cases before he was finally able to return to his home. He never recovered his belongings – and we never found the fraudster.

There are many other hardships for a legitimate owner. A fraudulent deed can prevent homeowners from selling their property, refinancing or accessing financial assistance programs.

To clear title, owners must file a quiet title lawsuit – a court action used to resolve disputes over who legally owns a property.

But quiet title cases are complex legal proceedings.

They require multiple filings, hearings and strict compliance with procedural rules. Even when fraud is obvious – for example, when a deed was signed by someone who was already deceased – courts generally require formal litigation to remove the cloud from the title.

Likewise, the legal process of notifying the defendant can be especially burdensome. Fraudsters often use fictitious names and addresses, making them difficult or impossible to locate. Even uncontested cases typically take months. If a defendant appears and disputes ownership, litigation can stretch for years.

Filing fees, service costs and other litigation expenses accumulate quickly. Hiring an attorney can cost several thousand dollars, and some victims have reported spending tens of thousands clearing title to their homes.

As for Kim Page, her case is still ongoing. After being locked out of her home, she had to move in with relatives for over a year, putting a strain on their relationship. She was eventually able to return to her home, but the legal dispute over ownership has not been resolved.

On top of that, she is facing a counter-lawsuit from the company that filed the fraudulent deed, requesting $50,000 for repairs the company made to the home while Page was locked out, along with property taxes and utility bills that the company says it paid to the county and utility companies on her behalf. The county opened an investigation, but it remains unresolved. As a result, she still has no idea who orchestrated the scheme.

While there are free legal services organizations to help, they have limited capacity, and income thresholds exclude some homeowners who still cannot afford private counsel.

Legal reforms likely won’t resolve systemic issues

Across the country, state legislatures have begun responding. Twenty-one have enacted deed fraud legislation, and 15 more have proposed it.

Another common intervention is fraud alert systems, which notify owners when any documents that impact the title of their property are recorded.

Other reforms increase notarial requirements or enhance criminal penalties.

These measures may deter some misconduct, but they do little to reduce the burden on victims once a fraudulent deed has been recorded.

In my assessment, meaningful reforms focus on empowering registers of deeds to substantively review suspicious documents before recording them; simplifying and expediting quiet title proceedings; and expanding civil remedies so victims can recover the costs associated with clearing their title.

Some jurisdictions like Texas and Florida have adopted streamlined procedures that allow victims to initiate quiet title actions using standardized forms with reduced fees. Others permit recorders, prosecutors or judges to act when fraud has already been established.

In Michigan, I am working with lawmakers and stakeholders to develop comprehensive legislation addressing these issues. Bills are expected to be introduced later this year.

At the same time, my clinic has begun exploring how technology can help identify fraudulent deeds already in the record. We are working with computer scientists to evaluate whether artificial intelligence tools could flag suspicious filings and potentially prevent fraudulent documents from being accepted in the future.

No property system can eliminate fraud entirely. Preventive and punitive measures may limit fraud, but they cannot eliminate the incentive to commit it. For fraudsters, the payoff can be substantial.

Conversations about the issue often begin and end with the mechanics of the crime or the procedural burdens victims face afterward. Far less attention is paid to the housing market conditions that make some communities especially vulnerable in the first place.

Page, now 42 and working as a transporter for Sinai-Grace Hospital, has been coping with the stress of legal proceedings for the past two years and living with a heart condition so serious that she got a defibrillator.

The longtime Detroiter is fed up – with the lack of police help to find the fraudster, as well as the court system. All she wants is to be the rightful owner of the home.

“Give me my house back,” Page said.

Detroit editor Eleanore Catolico contributed reporting.

Donovan McCarty, Director, Housing Justice Clinic at Michigan State University College of Law, Michigan State University

This article is republished from The Conversation under a Creative Commons license. Read the original article.

📰 Enjoying STM Daily News? Join the conversation!

💬 Leave a comment, share your thoughts, and subscribe to our newsletter for the latest stories, updates, and “News You Can Use This Moment!” delivered to your inbox.

Stay connected with STM Daily News!